The Fed, Fiscal Fights and FOMO

While the Fed’s next step and continuing fights around the nation’s deficit continue, it is not fear but FOMO that appears to have gripped markets with both the S&P 500 and NASDAQ reaching recent highs. We look to the bond/credit markets and other data to make sense of the current state of the economy.

FIVE THINGS YOU SHOULD KNOW

- Equity Markets – rallied this week with U.S. stocks (S&P 500) up 1.70% while international stocks (EAFE) gained 0.68%

- Fixed Income Markets – moved lower this week with investment grade bonds (AGG) down -1.33% and high yield bonds (JNK) down -0.34%

- Debt Ceiling – Talks this week between President Biden and House Speaker Kevin McCarthy suggested negotiations are just heating up, but the President did strike an optimistic tone commenting “there was an overwhelming consensus… that defaulting on the debt is simply not an option.” The president further reiterated to his team of negotiators on Friday that he is confident that Congress will act in time to prevent a US debt default.

- Commercial Real Estate Struggles – For the first time in over a decade, U.S. commercial real estate prices fell in the first quarter, an unwelcome risk to more banking stress considering lenders owned over 60% of the $3.6 trillion in outstanding commercial loans in Q4 of 2022. An increase in employees working from home continues to have a ripple effect on the commercial space.

- Key Insight – [VIDEO & ARTICLE] While the Fed’s next step and continuing fights around the nation’s deficit continue, it is not fear but FOMO that appears to have gripped markets with both the S&P 500 and NASDAQ reaching recent highs. We look to the bond/credit markets and other data to make sense of the current state of the economy.

INSIGHTS for INVESTORS

Credit Markets as the “Canary” in the Coal Mine

An old investing adage is that the market to watch is the bond market, as opposed to the more often discussed S&P 500 when it comes to its ability to predict what may lie ahead. This reasoning may be stronger than ever with the S&P 500 being so dominated these days by a handful of stocks, and two in particular (a handful of stocks, and two in particular together, now represent 14% of the S&P 500 market cap.).

The economy is of course much broader than a few large companies and so trying to deduce its future direction, while difficult to impossible in most respects, is at least made a bit more possible by looking at the credit markets. Unfortunately, even here the message seems a bit mixed at the moment … if trending in the wrong direction.

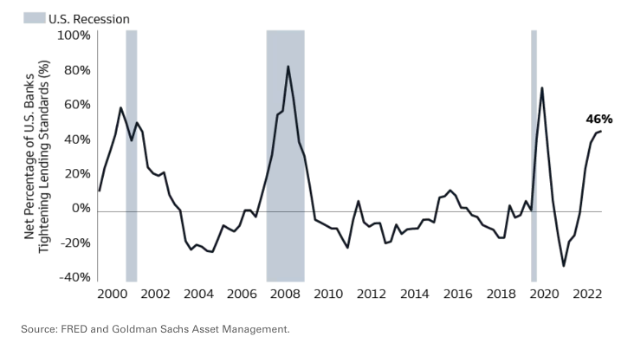

As noted by Goldman Sachs, “Credit conditions have tightened substantially since the onset of the Fed’s hiking cycle, but further deterioration following recent US bank stress remains subdued. The percentage of US banks reporting tighter C&I lending standards in the Fed’s April Senior Loan Officer Opinion Survey increased only marginally from 45% to 46%. The coast appears far from clear, but a credit-induced growth drag appears to have had a moderate impact thus far.”

Chart from May 8th 2023

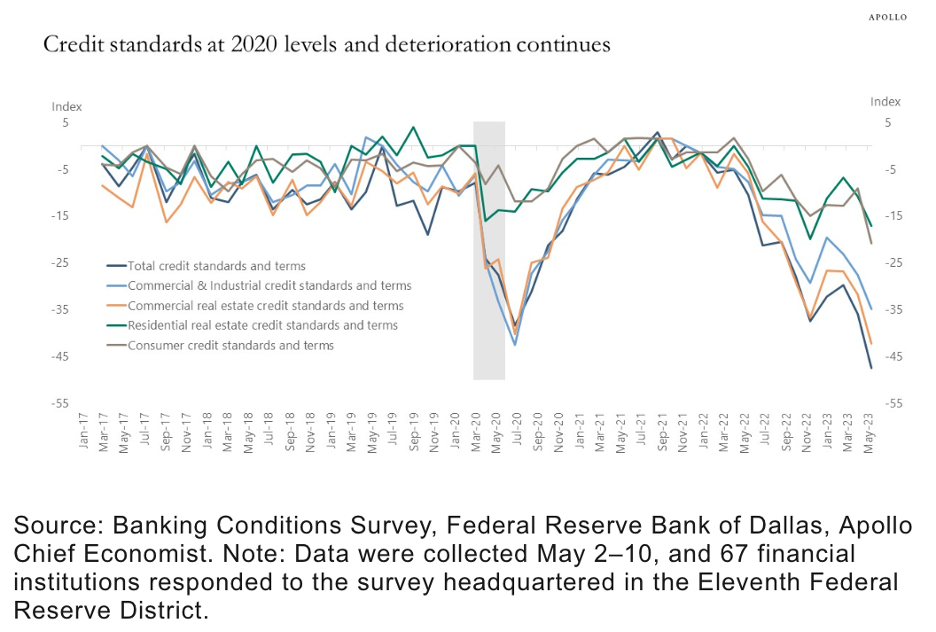

Other data from Apollo also reflects a troubling credit picture, much different than the survey responses above. They state, “A survey of 67 banks in the Dallas Fed district carried out in early May shows that credit standards have tightened significantly since SVB collapsed, and bank credit conditions are now at 2020 levels, and the deterioration continues, see chart below.

Combined with still tight IG and HY spreads, the Fed will look at this and conclude that tighter credit conditions are needed to get inflation down from the current 5% to the Fed’s 2% inflation target. Particularly in a situation where households are still sitting on plenty of cash, see also this new Fed working paper, which finds that consumers have plenty of excess savings left at least until the end of the year.”

As for actual guidance out of the Fed, multiple regional governors came out this week with statements regarding the need for further hikes (surprising markets) while Fed Chair Powell was a bit more vague, noting that current rate levels were already “restrictive” and that current banking conditions (as discussed above) are also “likely to weigh on economic growth.”

Chart from May 17th, 2023

Lastly, the yield curve continues to also suggest further economic slowdown, whether one looks at the 10-year vs. 2-year or 3-month treasuries, as all are solidly negative. Historically, such an inversion in rates is not a positive indicator for future economic growth in large part because of the disincentive around lending, which coupled with the conditions highlighted above are a real issue for the economy to work through.

Be Careful What you wish For

While markets and Americans continue to hope for some resolution to the current debt ceiling debate, Daryl Jones of Hedgeye had some noteworthy thoughts this week on the mixed messages being sent by the stock and bond markets. “Interestingly, through this whole debt ceiling debacle, the VIX has barely budged. It has basically been between 15 and 20 for the last month despite some legitimate concerns the U.S. could technically default. So, either equity risk (as measured by volatility) is missing something, or it has nailed that things will eventually get resolved.

On the other hand, the credit market is telling a slightly different story. In fact, as we highlight in the Chart of the Day, credit default swaps on U.S. Treasuries remain as elevated as we’ve ever seen. In fact, as of this morning CDS on 1-Year Treasuries remain north of 150bps, which is a level that surpasses what we saw during the previous debt ceiling showdown.

One reason for this divergence in market-based risk assessment is that equity risk could be getting it right that the debt ceiling impasse will be resolved, but then missing what comes after. As my colleague Josh Steiner has noted and highlighted in a few interesting articles this morning, there will likely be a deluge of Treasury issuance on the horizon after the debt ceiling is extended. Specifically, in the short run the U.S. government will have to massively replenish its “coffers” as cash has been drained down.

Some estimates have this funding requirement north of $1 trillion dollars through the end of the third quarter, which may be the effective equivalent of hiking by another 25bps. The derivative impact here could be that liquidity is drained, for a time, from the banking system, and short-term funding rates spike. Thus, the sustained heightened level of CDS on U.S. Treasuries makes sense when looking beyond the next couple of weeks.”

All of which is to say, an agreement may give the all-clear to more government spending but not necessarily to investors.

To “Land” or not to “Land”

Soft landing, hard landing, no landing … every day a new “call” and a new way to try to describe what may happen to the economy in the months ahead.

Tom Essaye had this nice take on the current fate/state of the economy. “Of the “Big Three” monthly economic reports, only one is flashing hard landing. Of the three most- important monthly economic re- ports (ISM Manufacturing PMI, ISM Services PMI and the Employment Report, only one, the ISM Manufacturing PMI, is pointing towards a hard landing. That PMI is solidly in contraction territory (below 50). However, both it and the ISM Services PMI rose from the previous month, implying some stability in those data sets. Looking at Jobs Adds (i.e. the monthly jobs report), clearly hiring has slowed from the breakneck pace of earlier this year, but monthly job adds in the 150k range is still very solid, and not at levels that imply a hard landing. What signals hard landing going forward? ISM Manufacturing PMI declining further, ISM Services PMI dropping below 50 in the next month or two, and job adds dropping below 150k starting next month.

What does that [Home Depot’s earnings report] all mean? It’s only one company’s insights, but it implies a soft landing for the economy, not a hard landing. Here’s why. Demand for housing “essentials” (again plumbing, electrical, etc.) remained “fine” implying the consumer has capacity to spend, but that same consumer is clearly pulling back on discretionary and “luxury” items (floors, counter tops, cabinets, etc.) Basically, that buying pattern hints at a consumer that still has money but is being more deliberate, thoughtful, and frugal (terms forgotten during the pandemic and recovery). That’s typical of a mild slowdown (soft landing) not a hard landing (where spending collapses all together).”

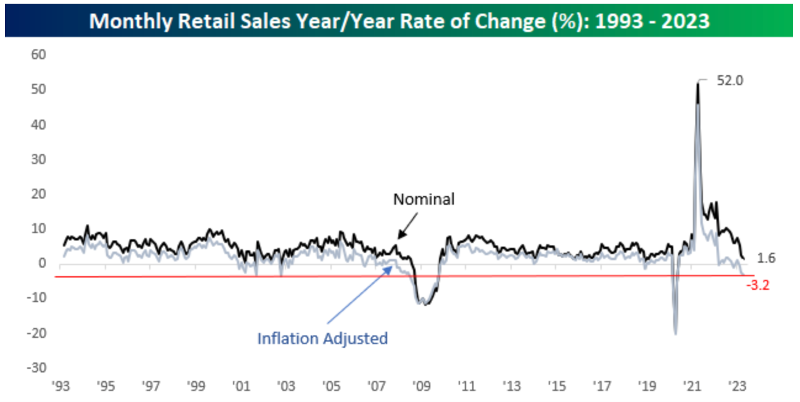

Bespoke’s concerns around a pending recession, and the likelihood of something more akin to a “hard landing,” focused on this week’s retail sales data. They noted, “We wanted to highlight reveal some concerning long-term trends. First, the chart below illustrates the six-month rolling average of the net number of sectors showing growth in monthly retail sales. The current reading, as of April, has only been weaker in a few other months, all of which occurred during the financial crisis. Negative readings have historically been associated with recessions as well.

Although sales remained positive in nominal terms, inflation-adjusted Retail Sales experienced a 3.2% year-over-year decline. This level of negativity has only been matched or exceeded in October 2002, during the Financial Crisis, and throughout the COVID pandemic. (data from https://www.bespokepremium.com/bespoke-report/the-bespoke-report-newsletter-6-16-23/)

Source: The Bespoke Report Newsletter. June 16, 2023

But perhaps, Hedgeye summed up the foolishness of people’s (most notably the Fed’s) historical attempts to predict the economy with their comment that “Time may or may not be a flat circle but soft-landing mongering remains timeless. Below is a selection of the soft-landing prognostications from 1989, 1999 and 2007. Enjoy …” (with accompanying graphic)

Discipline and Dividends

While many investors remain fearful, others are fully embracing FOMO (fear of missing out) sending the NASDAQ up 20% year-to-date to its 52-week high.

Perhaps our main takeaway from this recent market performance, as well as Essaye’s breakdown of the Home Depot earnings call above, is the likelihood for strong (relative or absolute) near-term performance of dividend paying stocks. A renewed focus on the necessities and related “soft” economy (not to be confused with soft landing) bodes well for value stocks which after a relatively strong 2022 have taken a backseat to tech stocks of late (see accompanying chart from Bespoke).

Summary

The reason the media and various pundits seem manic, is because they are. No one knows what lies ahead and as compelling as emotions and recency bias can be they do not help investors find any more clarity.

Counting on some degree of mean reversion, fading the crowd and/or one’s own emotions are not foolproof but are much more likely to keep you on course than other approaches.

You don’t need politicians or prognostications … you need a process.

Have a wonderful weekend,

Tim and the team at TEN Capital

DATA, JUST THE DATA

Data points this week included:

- U.S. Industrial Production – rose 0.5% month-over-month in April, above expectations for a flat reading. Production now sits +0.2% year-over-year

- U.S. Housing Starts – saw an unexpected increase of 2.2% in April for an annualized rate of 1.401 million. Single-family starts led the way hitting a 4-month high of 846,000

- U.S. Existing Home Sales – fell 3.4% in April to an annualized rate of 4.28 million, a 3-month low. Prices are also declining, with the median existing home price of $388,800 1.7% lower than 12 months prior.

- U.S. Jobless Claims – fell to 242,000 initial claims last week, down from the previous week’s 18-month high of 264,000. Continuing claims also fell last week to 1.799 million.

- U.S. Retail Sales – rose 0.4% in April, but below expectations of a 0.8% improvement. Core retail sales (ex. Auto, gas, building materials) rose 0.7% in a sign of sustained consumer demand.

- Eurozone Industrial Production – fell 4.1% in March for the most substantial decline in production since the pandemic-induced plunge.

Ten Capital Wealth Advisors is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is an SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Securities offered through Hightower Securities, LLC, Member FINRA/SIPC. brokercheck.finra.org

© 2025 Hightower Advisors. All Rights Reserved.